Moonshot Stocks & Mickey Mantle Cards

- 4 days ago

- 5 min read

Lessons We’ve Learned on Valuation & Supply vs. Demand

I have been asked a lot about SpaceX. Here are a couple of thoughts from living and working through a few moonshots and crashes in the Stock Market during my career. And there will be a few more monster-sized IPOs soon that crowds of investors will flock to, generating even more excitement and speculation.

To be very clear, I am not a rocket scientist. I have no idea what will ultimately happen to SpaceX (neither do the sharpest speculators buying shares). Elon Musk said he thought it might have a 10% chance of working out as a startup. Even for IPOs that work out fabulously well, never forget what an initial public offering is. Founders, insiders, and early private investors who know the business a lot better than the rest of us, choosing when to start selling their shares to the crowds.

What I do know is how to value a business, and the beautifully simple laws of supply and demand. We don’t have a horse in this race, since we are not investors in this stock. So I thought it might be eye-opening to jump in our time machine of good notes we keep and listen to somebody who was inside the technology stocks’ rocket ships of the late 90s. It will help make sure valuation is perfectly clear to any investor overlooking this same simple math today. Then, I’ll share my own favorite example of why I think supply versus demand is the most under-analyzed key factor in the direction of stocks’ prices. Whether it’s a piece of paper called a baseball card or a share of stock, the next price movement for each will be determined by whether there is more supply or more demand.

Valuation Matters A LOT

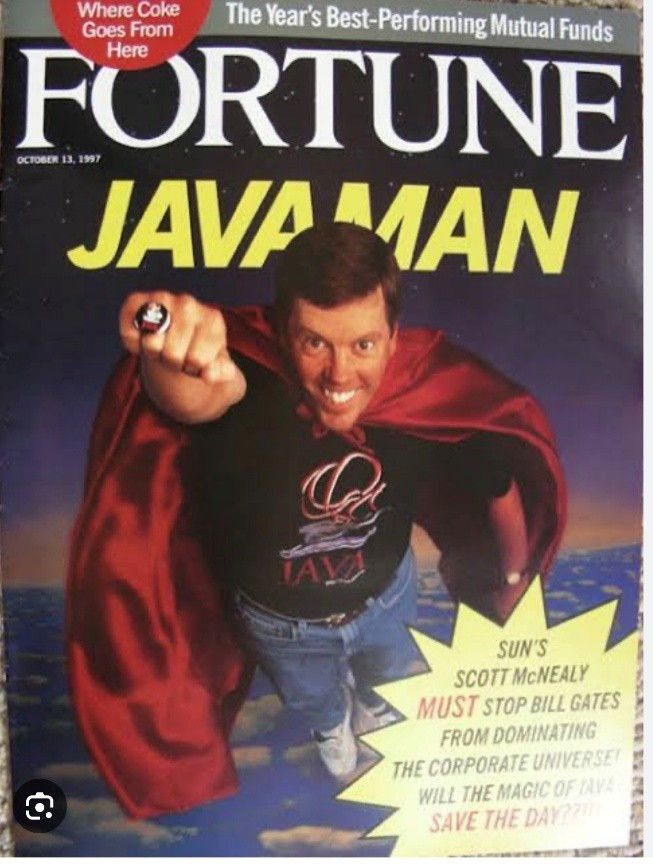

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I have zero cost of goods sold, which is very hard. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, and that you pay no taxes on your dividends - which is kind of illegal. And that assumes, with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having said that, would any of you like to still buy my stock at 10 times revenues? Do you realize how ridiculous those basic assumptions are? You don’t need any footnotes. What were you thinking?”

- Scott McNealy, CEO of Sun Microsystems

This quote came from one of the superheroes of the internet stock boom, when asked 25 years ago if he thought his own stock price, valued at 10 times revenue, was too good to be true.

Fast forward to now, SpaceX is currently being traded at more than 100 times its revenues.

Valuations will matter again. The laws of gravity can be temporarily suspended, the law of large numbers is more difficult to fly away from. It’s important to know that this IPO was very different than most. SpaceX only floated 4% of its shares. Typical IPOs are closer to 20%. So, there is a lot more supply coming to market down the road and more quickly per their covenants than most.

Supply vs. Demand Sets the Price

Meanwhile, back here on Earth, here is my favorite example to explain why more shares coming to the market or disappearing matter so much. This is a fun true story that anybody in your family can understand about the most famous piece of cardboard. While investment bankers confuse everybody else trying to explain the total addressable market across universes or galaxies, for a share of SpaceX stock.

The price for a piece of paper called a baseball card or a share of stock is set the same way – exactly when a bid meets an ask price. And the auctions can be influenced by the same greed, fear, and shenanigans. There was once a group of investors whose stated goal was to be “tops” in the business of “change-makers.” They were four brothers and sons of an entrepreneur. Their business was chewing gum. When they bought out a candy maker named Topps in 1938, they kept that name for their company.

Topps Chewing Gum Inc. tried many different things to compete with other manufacturers, like adding a comics wrapper or a magic trick. Then, a young salesman on staff named Sy Berger had an idea, but no design experience at all. So, he sat at his kitchen table in a tiny New York apartment with a ruler, scissors, and cardboard. He created a baseball card to insert with their piece of gum.

Starting in 1952, one piece of Topps gum came with six baseball cards in a wax wrapper. Demand was strong, and Berger suggested to the owners they make a second series of cards. They all sold well, so they kept making more. By the end of the season, there was a total set of 407 cards, released in six different series.

The increasing supply of that last series overwhelmed the slowing demand near the end of the baseball season. Stores stopped buying boxes from Topps, and extra inventory piled up.

Berger said, “I went around to carnivals and offered the packs for a penny a piece, and it got so bad I offered them at 10 for a penny.” After that, he could not even give them away. Nobody wanted them for free.

Even Topps thought so little of any future value that the company wanted to clear out all inventory to make room in their warehouse.

Berger rounded up the 1952 cards from that over-supplied last series, along with all those remaining boxes still unsold. He stuffed three garbage trucks full of them. He rented a barge to haul them all out to the Atlantic Ocean, where they were dumped. Berger later estimated it could have been 500 cases of the last series that he sunk. Each case has 24 boxes with 24 wax packs in each.

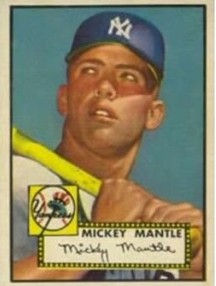

The last series, on the bottom of the ocean, are cards # 311 through # 407.

# 311 is Mickey Mantle. It became the Holy Grail of baseball cards. One of only six in the world with a mint grade recently sold for $12.6 million.

When I started on Wall Street in 1996, I never counted the number of different tickers available. I was not smart enough to measure supply yet, too busy trying to impress demand. I have learned many valuable lessons since then. The one that took me the longest is that informed simplicity is the Holy Grail card of investing.

Compared to the countless opinions on stocks, multiplied by exponentially growing digital information, could the most overlooked investment question be – how many of them are there?

More public companies have been eliminated from stock exchanges since 1996, than are available to trade today. The supply of different stocks to bid on has been almost cut in half over that time. Buybacks have shrunk share count even more. That’s no different than sinking cases of different kinds of pieces of paper called stocks to the bottom of the ocean floor.

If lots more shares start floating to the surface in new large IPOs, it could affect stock prices just like a change in supply vs. demand would in any other business.

From our friends at Bespoke Research, here is a chart we are keeping an eye on new supplies of shares coming to market.

We will remain focused on businesses already plenty profitable, and gushing free cash flow to reward stakeholders with what is already happening, rather than predicting what might happen.