Paradox Of Paper

- May 22, 2021

- 5 min read

Updated: Sep 19, 2024

The stated goal of this group of investors was to be “tops” in the business of “change-makers.” They were four brothers, and sons of an entrepreneur. Their business was chewing gum. When they bought out a candy maker named Topps, in 1938, they kept that name for their company.

Topps Chewing Gum Inc. tried many different things to compete with other manufacturers, like adding a comics wrapper, or a magic trick. Then, a young salesman on staff named Sy Berger had an idea, but no design experience at all. So, he sat at his kitchen table in a tiny New York apartment with a ruler, scissors and cardboard. He created a baseball card to insert with their piece of gum.

Starting in 1952, one piece of Topps gum came with six baseball cards, in a wax wrapper.

Demand was strong, and Berger suggested to the owners they make a second series of cards. They all sold well, so they kept making more. By the end of the season, there was a total set of 407 cards, released in six different series.

The increasing supply of that last series overwhelmed slowing demand near the end of the baseball season. Stores stopped buying boxes from Topps, and extra inventory piled up.

Berger said, “I went around to carnivals and offered the packs for a penny a piece, and it got so bad I offered them at 10 for a penny.” After that, he could not even give them away. Nobody wanted them for free.

Even Topps thought so little of any future value, that the company wanted to clear out all inventory to make room in their warehouse.

Berger rounded up the 1952 cards from that over-supplied last series, along with all those remaining boxes still unsold. He stuffed three garbage trucks full of them. He rented a barge to haul them all out to the Atlantic Ocean, where they were dumped. Berger later estimated it could have been 500 cases of the last series that he sunk. Each case has 24 boxes with 24 wax packs, in each.

The last series, on the bottom of the ocean, are cards # 311 through # 407.

# 311 is Mickey Mantle. It became the Holy Grail of baseball cards. One of only six in the world with a mint grade recently sold for $2.88 million.

When I started on Wall Street in 1996, I never counted the number of different tickers available. I was not smart enough to measure supply yet, too busy trying to impress demand. I have learned many valuable lessons, since then. The one that took me longest is that informed simplicity is the Holy Grail card of investing.

Compared to the countless opinions on stocks, multiplied by exponentially growing digital information, could the most overlooked investment question be – how many of them are there?

Oceans of private capital have soaked thousands of tickers that didn’t get swallowed up by mergers or go down the delisted drain of competition first. More public companies have been eliminated from stock exchanges since 1996, than are available to trade today.

Next to so many sophisticated reasons to question demand for stocks, the math that quietly changed a lot more, is the supply.

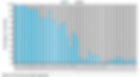

One of my favorite brains belongs to Michael Mauboussin. He dove deep into data on the relationship between public and private markets (chart below from his research, I highly recommend keeping an eye on all his work).

The ultimate success for a private startup used to mean it had to do an initial public offering (IPO) into shares of stock. Now, successful venture exits can take many different routes through mergers or acquisitions, and more rarely an IPO.

In the past, private companies eventually needed public markets for access to more capital, through an IPO, if they wanted to grow much bigger. Now, many businesses need less capital to scale. More buildings are digital, and many factories are in the cloud. At the same time, cash in the private markets is easier to find than ever before.

Adding jet fuel to the private market demand is performance chasing by large investors like public pensions – which find themselves on the wrong side of math. Liabilities grew faster than the traditional rates of return they expect from the public markets. So, they press the gas pedal on “alternative assets.” Many of these giant investment pools have doubled, tripled, or even quadrupled their allocations to private markets.

There are always going to be plenty of good prospects for private capital, and many exceptionally smart investors will find them. However, much of that new demand is coming from a crowd with bigger questions, not because they are finding better answers.

The caravans of unicorn hunters are paying top dollar to exotic venture ranches breeding and feeding. So, private companies keep getting bigger. This left column has all the tickers crammed in, of publicly traded stocks worth less than $1 billion. On the right, is the number of private companies valued more than $1 billion.

The demand for more upside potential has decreased the number of Mickey Mantle debuts in the Stock Market. This is a tremendous opportunity for individual investors acquiring the highest quality vintage stock market paper, in limited supply.

Potentially widening the data set of mispricing, during any panic, allocators do not get to choose what they want to sell. They sell what the can. Most private investments are illiquid. Big companies’ publicly traded shares can be turned into cash, anytime. So, not only are new shares not being printed at the same rate, but a lot of the oldest stock certificates are disappearing.

There are a lot of very good reasons why stocks will go down. Bad things will happen to the economy, then worse things. All of those problems are crashed into by so many different black swan events now, that only a polka-dotted swan would be a surprise anymore. But, the publicly traded shares that stand the test of all those times, do so for longer lasting reasons.

Brian Reynolds was my favorite quiet voice, back when I ran a hedge fund. He relentlessly measured numbers (like his chart above), rather than calling shots. What I love about math is that it leaves no room for opinions.

I closed the hedge fund several years ago, after a successful run, because I wanted a simpler answer to a question about all paper assets – how do we know what’s real?

More humble math revealed to me what has, and will, last so much longer. Increasing dividends of the highest quality have a track record that no trading strategy can match.

Endless debates about re-allocating from growth to income, then back and forth, overlook the most important real question for most families’ nest eggs – how do we achieve growth OF income?

Rising dividends can be held in our hands, to know what is real. It is free cash flow income, not a withdrawal rate from a hoped-for projection. Financial freedom comes from growth of income. Anxiety comes from hoping there will be enough appreciation to withdraw from.

Companies that have an advantage that is expanding, while increasing free cash flow, can reward shareholders with rising dividends. Nothing has changed that formula for success. But, what if old-fashioned shareholders’ own advantage may have improved?

There is growing demand from investors to be the “tops” and find “change makers,” just like those chewing gum investors almost a hundred years ago. As hopes in the private markets grow, boxes of old stock certificates left over in the public markets, can look less appealing. The paradox of that vintage paper is that when fewer people believe in it, the limited supply of consistently rising dividends may become even more valuable.